You have probably already noticed that your fire insurance premium is likely to increase on the expiry date of your contract.

You may legitimately wonder why this is the case. Is it an automatic price indexation or are there other explanations? How is the price of fire insurance calculated in Belgium?

In reality, several factors influence the amount of your premium, some of which are completely beyond your control.

Here we explain the five main factors that can affect your fire insurance premiums.

1. The ABEX insurance index: the most influential factor

The ABEX index (Association Belge des Experts), or ABEX Index, is one of the main parameters that directly influences yourhomeowner's fire insurance premium. Created in 1963, this index is updated twice a year and uses the index 1, assigned on January 1, 1914, as its historical reference. It measures changes in the cost of building homes and private dwellings in Belgium, based on a national average.

Although it can be compared to inflation, the ABEX index is unique in nature. It focuses solely on the construction sector and is therefore influenced by two main factors: labor costs and material prices.

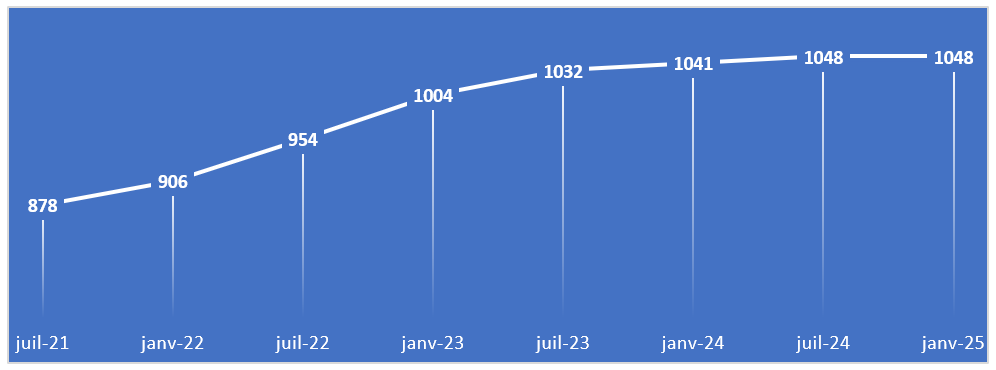

Recent changes in the ABEX insurance index:

After a sharp increase between 2022 and 2023 (+10.8%), mainly due to widespread inflation and rising construction material costs—fueled by higher energy prices and raw material shortages linked in particular to the war in Ukraine—the ABEX 2024 index saw its growth slow in 2024 (+3.7%). Notably, it has remained stable over the last six months, which has not happened for nearly 10 years! The ABEX 2025 index currently stands at 1048.

These changes in the index have an almost immediate impact on the amount of your insurance premiums.

Concrete example of the impact of the ABEX index on the premium:

- Coverage implemented in January 2022;

- Value taken into account (= replacement value): €300,000;

- Net premium: €300

=> In January 2024, with an ABEX index of 1,041 instead of 906, the insured amount increases from €300,000 to €344,701, correspondingly increasing the premium from €300 to €344.7 in two years.

These index adjustments therefore result in a proportional increase in your premium, even if you have not made any changes to your contract.

2. The insurer's overall claims history

Each insurer sets its premiums based on its own claims history. If a company has had to pay out an unusually high number of claims over a given period, it may be forced to raise its rates in order to remain profitable.

Compensation paid for these events is spread across all policyholders. Therefore, even if you have never filed a claim with your insurance company, you could be affected by its overall results. This is the mutualization mechanism, a basic principle of how the insurance sector works: policyholders' premiums help cover the costs associated with all claims.

3. The increase in natural disasters: impact on the price of your insurance

Climate change is intensifying the frequency and severity of natural disasters, which has a direct impact on risks and, therefore, on insurance premiums. Globally, claims related to natural disasters cost hundreds of billions of euros each year. In fact, 2024 was one of the three most expensive years since 1980 for reinsurers.

In Belgium, the 2021 floods in Wallonia, which cost more than €2 billion, highlighted the need for Belgian insurers to better prepare for these growing risks, in particular by taking advantage of the mutualization mechanism through a general rate increase.

For more information, see our article "Your insurance policies and the challenge of climate change,"which you can read to better understand the impact of climate change on your insurance policies.

4. Tax changes: impact on the price of your insurance

In Belgium, insurance premiums include a mandatory tax and, in most cases, contributions, which may change in line with new regulatory or legal provisions. Any change in the percentage of these taxes and contributions may be directly reflected in your premium notice.

In concrete terms, the tax varies depending on the type of contract, but it is generally 2% or 4.4% for life insurance and 9.25% for most other risks (fire, auto liability, etc.).

Contributions are included in the premium to cover specific obligations or mechanisms, such as the 6.5% contribution to the Disaster Fund under fire insurance, or the 17.85% contribution to the Common Guarantee Fund for auto liability insurance.

Although these rates have remained relatively stable in recent years, any decision to increase these taxes or contributions would automatically lead to higher premiums for all policyholders.

5. Other parameters specific to your home

In addition to the factors mentioned above, which are generally beyond your control, your insurance premium may also increase in a more "objective" manner depending on changes made to your home, such as:

- In the event of expansion or improvement work —if you add an extension, a swimming pool, or carry out major renovations—the value of your property increases, and so does the insured amount.

- If you install specific equipment —solar panels, heat pumps, or other equipment—you may need specific warranties that could increase your premium.

- If the property's use changes —for example, from a family home to a rental property—this may also affect coverage and rates.

Conclusion: consult your RGF specialist to review your insurance policies.

The independence of the RGF Group allows us to defend your interests above all else. We help you find not only the best coverage, but also the best rate for your situation.

The insurance industry is highly competitive, and that works to your advantage. Our role is to leverage this competition to offer you the solution that best suits your needs and your budget.

As you can see, insurance that seemed ideal at the time of purchase may no longer be so after a few years, due to the factors mentioned above.

Please note that in the event of a rate increase, you can cancel and transfer your contract without notice. We offer you the opportunity to carry out a comparative analysis of your insurance contracts with an RGF specialist in order to guarantee you the best protection at the best price over the years.

By Julie G

I would like a free quote

Fill out the form below to receive a personalized offer: