Group insurance is an extra-legal benefit offered by companies to their employees, just like a company car or meal vouchers.

Group insurance is taken out by the employer for some or all of its employees. The contributions paid by the employer accumulate over the years to form a pension fund that will be paid to employees when they retire. In addition to a lump sum available upon retirement, other options may be included in group insurance, such as: death benefit, guaranteed income in the event of incapacity for work, and hospitalization insurance.

Benefits for your business:

the premiums are fully deductible for your company,

you save on employer contributions.

As legislation is constantly changing, RGF analyzes your needs and offers you the solutions best suited to your organization.

Group insurance in Belgium

Your company makes regular contributions for its employees who are members of the group insurance plan. Each year, these amounts accumulate and form a pension fund. Premiums can be determined

✅ Either as a percentage of remuneration

✅ Either based on a monthly flat rate

✅ Either based on a defined pension capital (target to be achieved)

In addition, your employees can also contribute to their group insurance by making personal contributions.

Once you have determined the budget you wish to allocate to your staff, you choose the financing method: Branch 21 (guaranteed capital) or Branch 23 (equity and bond funds).

Group insurance allows your employees to take advances or pledge pension funds to purchase, build, improve, repair, or convert real estate.

Online group insurance Why RGF?

The RGF Group analyzes your situation objectively and seeks the best solution for your company.

RGF, an independent organization specializing in employee benefits, guarantees you:

Experience, expertise, know-how, and creativity

An independent and objective analysis of your plan

Regular assistance with contract management (staff onboarding/offboarding, plan renewal, updated social security contributions, etc.)

Individual interviews (social review) for any employee who wishes to participate

Support for real estate projects (amortizable/bullet loans)

Partnership: access to our other departments (insurance, banking, loans, financial and estate planning, etc.)

Support for the person responsible for personnel (we are your intermediary and take care of everything)

Contributions paid into the group insurance plan are fully deductible as business expenses (attractive tax treatment).

Attractive compensation

An optimized group insurance policy is an effective tool for attracting new talent and retaining your employees in the long term (leveraging human resources).

A model for growth

Your company pays lower fees, and group insurance provides a gross/net ratio that is more than double. This makes it more advantageous than a pay raise.

The benefits for your employees

Tax benefit

As an employee, you build up a supplementary pension plan to supplement your statutory pension. The capital from your extra-legal pension that you receive through your group insurance is taxed at a much lower rate than your salary (± 20% compared to ± 50%).

Purchase and mortgage

Employees may ask you for an advance on their group insurance for a real estate purchase, renovation, or repayment of an existing mortgage anywhere in the European Economic Area (EEA).

This way, workers protect their families in the event of death and can include coverage against loss of income due to illness or accident in their group insurance contract.

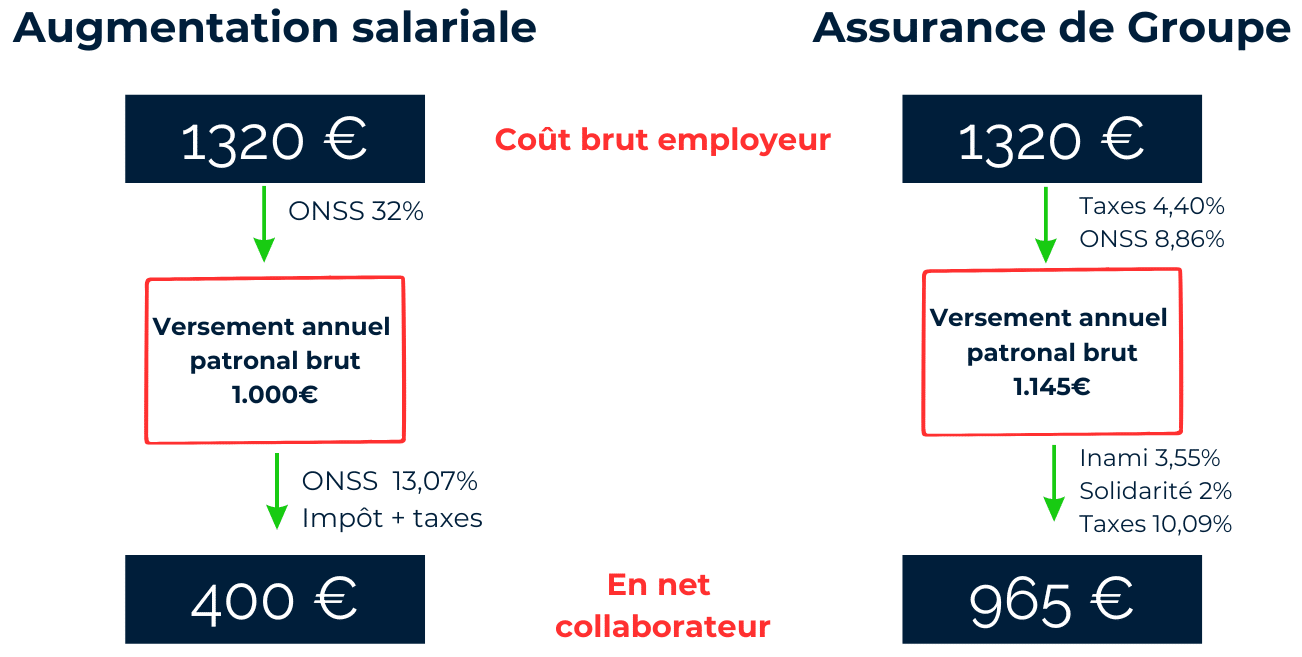

Group insurance in figures

In summary:

Group insurance costs you less than a traditional salary increase, and your employees enjoy greater purchasing power.

In the example above, paying a group insurance premium rather than an equivalent salary increase offers a clear advantage for your employees and reduces your payroll costs.

When you retire, you have the option of paying out the amount saved in your supplementary pension plan in two different ways: either as a lump sum or as an annuity.

How is your group insurance capital taxed?

Lump sum payment

Initially, your capital is taxed at a solidarity contribution rate of 2% (1% for capital below €24 , 790) and an INAMI contribution rate of 3.55%. Next, the withholding tax rate varies depending on your retirement age (early retirement or not, full 45-year career, etc.).

For example, if the capital is paid out at the legal retirement age (67) and you have remained active for the last three years, you will benefit from a favorable tax rate of 10% on the premiums paid by your employer.

With regard to your personal contributions, it is important to take into account the date of January 1, 1993. All contributions made before this date are taxed at a rate of 16.66%, and all contributions made after this date are taxed at a rate of 10.09%.

Please note, however, that you cannot claim your group insurance capital before reaching the legal retirement age. To find out about taxation and the different tax rates for your supplementary pension payments, see our article.

The rules governing your supplementary pension plan may provide forthe payment ofyour capital in the form of lifetime annuities. These may be monthly, quarterly, half-yearly, or annual. They are added to the amount of your statutory pension as professional income. They are therefore taxed at the marginal tax rate after deduction of the INAMI contribution of 3.55%.

In summary, withdrawals in the form of an annuity are subject to a progressive tax rate. The tax regime can therefore be advantageous for lower incomes.

You can also request that your entire capital be taxed at once and convert it partially or totally into an annuity. This allows you to benefit from more favorable tax treatment:

☑️ Your tax return must show an annuity equal to 3% of the net capital.

☑️ This base as income from movable property is taxed at a fixed rate of 30% + municipal tax.

What happens to my group insurance if I change employers?

Throughout your professional career, you may be dismissed or resign. In this case, your group insurance capital is not lost, but your former employer will no longer pay the premiums associated with it. You then have several options for your accumulated pension capital:

✅ You can leave the amount accrued with your former employer's insurer. Premiums are no longer paid, and interest continues to accrue on the capital already accumulated until you retire. The terms and conditions of your pension plan are guaranteed. However, you may lose your death benefit coverage before retirement.

✅ You can leave the amount already saved in your former employer's group insurance plan and take out death coverage for an equivalent amount. Your supplementary pension capital will be lower in the long term. In return, your insurer guarantees to pay the saved reserves to the designated person or persons in the event of premature death.

✅ You can transfer the amount accumulated in your supplementary pension plan to your new employer's insurer. This is only possible if your new employer takes out group insurance for its employees.

✅ You can transfer the capital of your pension to a host structure (if your former employer's insurer provides one). This is a separate structure that is independent of the initial pension plan. The guaranteed interest rate is often lower.

✅ You can transfer your savings capital to an AR 69 retirement institution. This is an insurance company that shares profits among all members in proportion to the amount of their reserves. This type of institution reduces management fees.

This rule defines the maximum amount you can save in your supplementary pension plan without losing your tax benefit. This benefit provides for the tax deduction of premiums paid by your employer or by you as an employee.

To benefit from this deduction, the tax authorities have introduced the 80% rule. This law sets a maximum amount for premiums that cannot be exceeded. If you exceed this amount, your group insurance premiums will no longer be deductible.

Calculation of the 80% rule

The principle behind this rule is simple and works as follows: your supplementary pension from the second pillar, combined with your statutory pension, cannot exceed 80% of your last gross annual salary. It should be noted that private pension savings from the third pillar are not taken into account under this rule.

Can you take out group insurance as a self-employed person?

As the head of a company, you can take out group insurance or an individual pension plan. EIP through your company. Your company can then set up a supplementary pension for all its executives while benefiting from tax advantages for the self-employed (deductible premiums and supplementary guarantees).

Among other things, if you are self-employed without a company, you can save for your supplementary pension with a PLCI. This is the abbreviation for free supplementary pension for self-employed workers. This means you pay less in charges thanks to a tax system that reduces your taxes and social security contributions.

Advance on group insurance for a purchase or mortgage?

As an employer, you can motivate your employees with group insurance tailored to finance their private real estate projects. The reserves accumulated in their pension plans can be used to purchase, build, or renovate a home.

You can then stipulate in your pension regulations that you offer your employees the option of taking an advance. This advance can also be used to repay an existing mortgage.

This advance is a loan against the reserves of the supplemental pension plan. The employee must pay interest on the amount they decide to withdraw. They can then choose to pay annual interest or capitalize it. In other words:

✅ Either you take an advance and pay a fixed or variable interest rate each year, depending on your contract.

✅ Either you capitalize your advance and do not pay interest each year. Your advance and the interest owed will be deducted when your pension capital is paid out.

In both cases, employees can benefit from an interest deduction on group insurance. The annual interest payment can be deducted each year, but also when the advance is repaid or when your pension reserve is paid out.

The employee may also pledge their insurance contract to a bank or replenish their capital with a bullet loan based on projected capital (investments in Luxembourg, real estate project, etc.).

Group insurance offers many advantages for both employers and their employees. Premiums paid are 100% tax deductible, and employers benefit from additional coverage.

Your group insurance capital can be paid out as an early retirement pension from the age of 60. However, to benefit from favorable taxation, you must remain active until the legal retirement age.

We use cookies and similar technologies for various reasons. Some are essential for the site to function, while others, such as analytics or advertising cookies, improve our services and personalize your experience.

You can accept all cookies, refuse non-essential cookies, or customize your preferences. You can change your choice at any time via the cookie settings. For more information, see our Cookie Policy.

Necessary for navigation and functional

Always active

Strictly necessary and functional cookies ensure the proper functioning of the site, enable navigation, secure access, and remember your preferences. Without them, certain features may be impaired or inaccessible.

Cookies de préférences

Ces cookies permettent de mémoriser vos préférences de navigation, notamment la langue choisie, afin de personnaliser votre expérience sur le site.

Cookies statistiques et d'analyse

Ces cookies collectent des informations anonymes sur la manière dont les visiteurs utilisent le site, afin de mesurer la fréquentation, analyser les pages consultées et améliorer l'ergonomie du site.Le stockage ou l’accès technique qui est utilisé exclusivement dans des finalités statistiques anonymes. En l’absence d’une assignation à comparaître, d’une conformité volontaire de la part de votre fournisseur d’accès à internet ou d’enregistrements supplémentaires provenant d’une tierce partie, les informations stockées ou extraites à cette seule fin ne peuvent généralement pas être utilisées pour vous identifier.

Cookies marketing et publicitaires

Ces cookies sont utilisés pour mesurer l'efficacité des campagnes publicitaires, suivre les conversions et proposer des contenus adaptés à vos centres d'intérêt.