Recent economic events, particularly decisions made across the Atlantic concerning import tariffs on goods entering the United States, have caused some nervousness on the financial markets.

In this type of situation, knee-jerk reactions often take precedence over a rational assessment of economic fundamentals. The prevailing nervousness fuels uncertainty, and the temptation to "get out" or "secure" one's capital becomes understandable. However, decisions made in the heat of the moment are rarely the most sensible ones. It is precisely at times like these that we need to go back to basics: investment horizon, diversification, regularity... and keeping a cool head.

An interesting parallel can be drawn with the Covid crisis. InMarch 2020, within a matter of weeks, global indices fell by more than 30%. Investors were faced with a completely unprecedented event with major health, economic, and social implications. And yet... it took less than a year to return to pre-crisis levels, and barely more than that to exceed them by a wide margin.

Those who gave in to panic often crystallized their losses. Conversely, those who remained invested—or better yet, those who maintained a recurring investment strategy during the downturn—benefited fully from the rebound. They bought at a good price, strengthened their positions, and improved their overall returns.

The lesson is well known, but worth repeating: markets correct, sometimes sharply, but always end up rebounding. And what we are currently experiencing is no exception.

Recurrence: your best ally in times of volatility

How to invest in the financial markets? Regular savings! This isn't just a "convenient" solution, it's a genuine investment strategy in its own right, which takes advantage of market movements rather than "suffering" them.

By investing the same amount each month, you benefit from a mechanism known as "dollar-cost averaging." In simple terms, when the markets are high, you buy a little less, but when they fall, you buy more. Over the long term, this allows you to optimize the average purchase price of your investments.

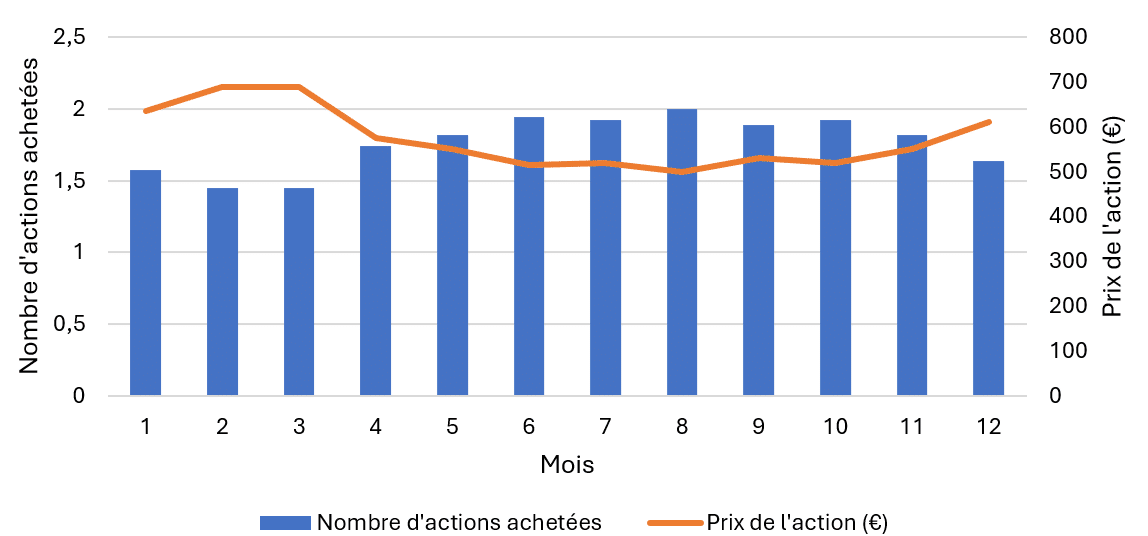

Let's take a concrete example based on the valuation of a share over the course of a year. Here are the prices observed from January to December:

Let's imagine two investment strategies:

- Investor A invests €12,000 in a single payment in January.

- Investor B invests €1,000 each month, from January to December. He therefore buys more or fewer shares depending on the value of the asset at the time of purchase, which gives the following result:

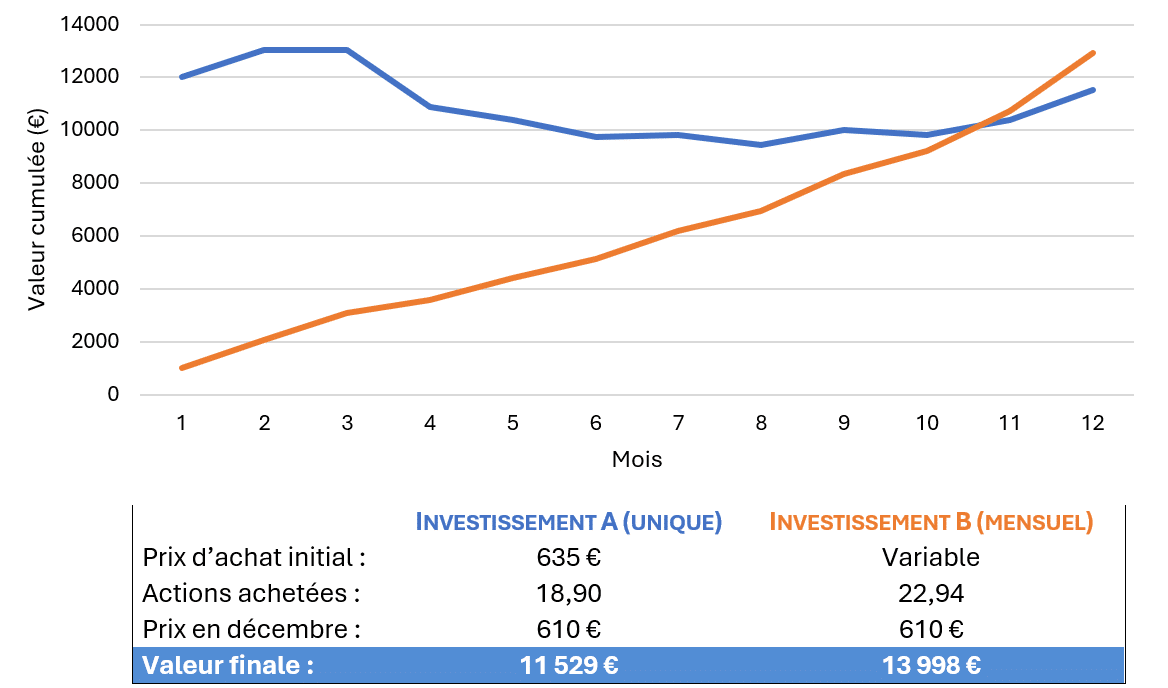

Year-end result:

Despite a decline in the share price between January and December, investors who saved each month ended up with a positive final value (+€1,998), which was nearly €2,500 higher than those who invested everything at the outset and suffered a loss (-€471).

Why is there a difference?

Because investor B bought more shares during the months when the price was lower (May, June, August, etc.), which lowered their average purchase price. At the end-of-year revaluation, they benefit from a positive mechanical effect on all of their shares.

Key takeaways:

- In times of fluctuation, gradual investment often helps to optimize the final return.

- It emotionally protects investors from stress peaks.

- It limits the risk of poor timing, particularly when the market is irregular or difficult to read.

Monthly savings are therefore not only accessible and disciplined, but also strategically relevant, especially in an uncertain and volatile environment.

Note that this mechanism can also be used when investing large amounts of capital. Some organizations offer the option of " drip feeding , " which involves gradually investing capital in a series of payments spread out over time, generally over a period of 6 to 24 months.

In practical terms, the total amount is invested at the outset, but only a fraction is actually invested in the markets each month, according to a pre-established schedule. This system automatically spreads the risk of entering the markets, avoiding investing all of the capital at a potentially unfavorable time.

Diversification: the second pillar of your peace of mind

In the current climate, diversification is not just good practice—it is a necessity. Markets operate in a complex environment marked by regional, sectoral, and political differences. Now more than ever, the key is not to put all your eggs in one basket.

Diversifying your portfolio means, above all, spreading your investments across several types of assets: stocks for long-term growth, bonds for stability and income, flexible funds for adaptability, and sometimes specific themes such as healthcare, energy transition, or new technologies. This allocation helps smooth out performance, reduce overall volatility, and adapt the strategy to different economic cycles.

Geographic diversification is equally essential. Each region has its strengths and weaknesses: the United States excels in technological dynamism, but is sometimes highly concentrated; Europe offers more reasonable valuations, driven by solid sectors such as luxury goods and healthcare; emerging countries, although more volatile, remain powerful drivers of long-term growth. By combining these regions, investors avoid dependence on a single economic engine and increase their chances of seizing opportunities where they arise, while cushioning the impact of localized shocks.

Do not exit markets without reason

Selling during a downturn simply means accepting a loss. And exiting the markets when they are falling also means missing out on the subsequent rebound. One of the most common reflexes is to "get out and wait for the market to recover." But in reality, markets often rebound faster than we think. The risk? Missing out on the best days... the ones that make all the difference to long-term performance.

In reality, the amount of time spent in the markets is generally more decisive than the timing of entry or exit. Unless there is an immediate need for liquidity, it is better to remain invested and let the long-term strategy do its work.

In conclusion: 3 situations, 3 strategies

- You are already invested: if your investment horizon is medium/long term, hold on, the markets will eventually rebound.

- You save every month: keep going, or even consider strengthening your positions, as it is during the most volatile periods that this strategy yields the best results.

- You have capital to invest : there's no need to invest it all at once. Consider "drip feeding": investing in stages, on a regular basis, to limit the impact of the entry point.

Need to discuss it?

Your RGF advisors are available to review your situation, reassess your overall strategy, or simply answer your questions.

By Julie G

I would like a free quote

Fill out the form below to receive a personalized offer: